Rescue Your Business

(Note: the site TheBusinessRescue.com directs here)

Here’s a 14-point plan for rescuing your business. If your business is suffering from declining revenues – perhaps due to COVID-19 – you should implement these steps immediately.

Before we get to the specific steps, there are three general principles:

- Be proactive in solving problems. Assume your creditors / suppliers / customers are NOT going to contact you, and that YOU need to pick up the phone and contact them.

- When you contact someone to whom you owe money or who owes you money, work to find a middle ground that eases the pain for both parties.

- “Something is better than nothing.” This works both ways – you can use this idea when negotiating with creditors and with people and businesses that owe you money.

Step 1: Communicate.

Send an email to all your customers and vendors.

- “We’re okay.”

- “This is what we are doing…”

- I wrote a separate blog post on how to write this email in 15 minutes or less. Basically, the strategy is to copy what the big guys are doing and tweak it for your business and situation.

- Send a weekly update until the crisis is over, then transition this newsletter to something more positive: “Here are the cool things we are doing now…”

Step 2: Propose a “Debt Holiday” to all your creditors.

- Some great and powerful justifying language you can use is “In order to save the company…” This works because your creditors do not want you to go out of business!

- Another powerful phrase is “We are doing the same thing with our customers.” See step 3 below.

- Some terms you might be work out:

- If you regularly make monthly payments on something, offer to pay a smaller amount monthly (and extend the term of your payments).

- Offer to pay off something in advance, and get a

big discount – ask for 25 or 30 percent and negotiate down to 20 or 25 percent.

- Let’s say you had 10 payments left on something at $500 a month. Offer to pay it off in five payments of $750 each.

- Break a one-time expense you were planning to pay off all at once into monthly payments. These payments should be interest-free.

- If you regularly buy and pay for something on “Net

30” terms or similar, renegotiate this to a revolving line of credit.

- Offer to pay at least 20% of your balance each month. Example, you spend between $800 and $1,200 a month on some supplies. Offer to pay $200 on your $1,000 balance this month; $342 on your $1,712 balance (bought $912 more) next month; $502 on your $2,510 balance (bought $1,140) the third month; and so on.

- This works especially well if the amount you spend monthly fluctuates.

- If your cash flow can sustain it, you can always pay more than 20% in a given month.

Step 3: Collect as much debt as possible.

- Some great and powerful justifying language you can use is “In order to save the company…” This works because your happy and satisfied customers do not want you to go out of business!

- The reality is that many businesses, instead of

following the proactive principles we have outlined, will try to “hide” from

their creditors as long as they can. These businesses will appreciate

you reaching out to them to work something out.

- Remember, you are trying to find some middle ground that eases the pain for both parties. WIN-WIN: lowering the size of their payments while guaranteeing you some portion of the income.

- Get creative. Propose using some of the terms outlined in step 2, only from a creditor’s perspective.

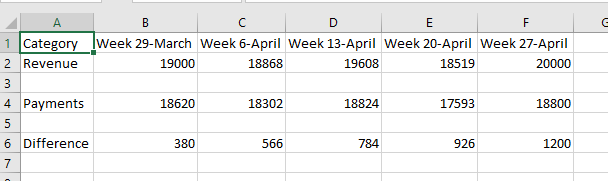

Step 4: Document your company’s cash flow plan.

- This is a very simple spreadsheet …use Excel or

Google Sheets.

- I recommend YOU, the business owner, do this – DO NOT hand it off to your accountant.

- Weekly cash flow is more precise, but you could do monthly if that makes sense to you.

- We have found an 8-week cash flow works well, but you can do as few as 6 weeks and as many as 13 or more.

- Your fields at the top of the spreadsheet are your time periods, week by week or month by month.

- The rows in your spreadsheet are the sources of revenue (sales and collection of receivables), and the outgoing payments (remember payroll, taxes, all your regular fixed costs).

- Subtotal revenue and payments.

- Last row is the difference between revenue and payments (revenue minus payments).

- After you do the cash flow the first time, you may need to go back to creditors and customers and move some payments around to make sure that outgoing payments each week/month are less than incoming revenues.

- Update the cash flow each week so you can proactively make adjustments as you go along.

Step 5: Secure the value in your company.

- Use a technique called “Invoice Out” to move the

ownership of your assets to a new LLC, and then lease the assets back from the new

LLC.

- This can shield your assets from creditors.

- As long as your company is not currently embroiled in litigation, this should be legal.

- Please consult your legal and tax advisors for more information.

Step 6: Have employees work from home whenever and wherever possible.

- This a really a long-term strategy that you can start now.

- If “office” employees can permanently work from

home, eventually you will need little to no office space, and can save on rent,

utilities, etc. Huge savings on overhead are possible.

- If you have to have a physical location to meet with B2B customers, or for “image” purposes, consider using a shared office such as a Regus.

- A permissive “remote work” policy allows you to hire the best workers from across the United States, or even the entire world, instead of being limited to the employees who are within reasonable commuting distance (< 25 miles) from your office.

Step 7: Convert Bank Credit Lines to Long-Term Loans

- As credit lines generally are callable and long-term loans generally are not, it should be instantly obvious how this can save your company when the financial waters are choppy.

- Long-term loans usually have lower interest rates.

- Usually when you do the conversion, you can pull out some extra cash.

- When everything gets back to “normal” (or the “new normal”), you can go back and apply for another line of credit, which you will probably get.

Step 8: Negotiate payment freezes on your loans with banks.

- Ask if you can hit the “pause” button and suspend payments for 60 – 90 – 120 – 180 days. No additional interest accrues, no late fees, etc. You’ll start making payments again as scheduled when the “pause” ends, and you will make all of the scheduled payments (although it will take you 60 – 90 – 120 – 180 more days than originally planned).

Step 9: Reduce Overhead.

- Eliminate any non-essential overhead that does not contribute to revenue.

- Does it make you money or

is it “nice to have”?

- Examples: any subscriptions (like cable TV, water cooler, etc.)

- Any “premium” level of a product or service when the regular product/level would work just as well.

Step 10: Negotiate a lease-freeze with your landlord.

- The landlord may be very willing to make you a deal because he wants to retain you long-term in what is, or will shortly become, a crappy commercial real estate market.

- The longer and better relationship you have with your landlord, the more you can ask for.

- Start out by asking for six months rent-free and see where it goes. Worst that can happen is the landlord says “no” and counter-offers.

Step 11: Re-negotiate your mortgage.

- Put the owned assets into a new legal entity (see Step 5), which gets a new mortgage, and then lease the assets back from the new entity.

- The new mortgage can be for a longer term than the original in order to lower the payments.

- The new mortgage can be for a greater amount

than the original in order to pull out some cash.

- You could then keep the cash in the new entity and lower your company’s lease payments for a time (see steps 2 and 10), using the cash to pay the difference between the mortgage payment and the lease payment.

Step 12: Ask taxing authorities for a stay of payments.

- Use the tactics discussed in steps 2 and others to reduce the size of your tax payments.

Step 13: Reduce company vehicle payments.

- You may have already negotiated something in step 2.

- If you lease vehicles, will you need fewer vehicles temporarily while business is slow? Maybe you can end a few leases early. Remember, if you are proactive, EVERYTHING IS NEGOTIABLE.

- Can you reduce your vehicle insurance payments by reducing the coverage on “parked” or “mothballed” vehicles? Ask your insurance agent or broker.

Step 14: Reduce insurance payments.

- Ask your agent or broker what is possible. Can you put some payments on “pause”?

- Ask your current agent or broker to re-quote you based on current conditions.

- Now is a perfect time to re-bid your insurance coverage with a different company or broker.

What if you are on your creditor’s “naughty” list?

One issue distressed businesses often face, particularly if things have been going south for a while, is they have exhausted their creditors’ patience and goodwill. As a result, relationships with creditors have deteriorated to the point where any attempt to ask for some leniency is met with a stone wall.

One solution to this problem is to bring in a consultant who can talk with creditors and say the following:

“I am thinking about getting involved in this business. Clearly, you know something is not right. Can you give me 4 to 6 weeks, and I’ll report back to you on our plan?”

Conclusion

If revenues are declining, and your business needs rescuing, there are steps you can take to financially engineer your business and start to dig your way out of trouble and back to profitability. Remember,

- Be proactive.

- Find WIN-WIN solutions to problems.

- Something is always better than nothing.